AI, sustainability and your investments

Related links

Read the 2025 Responsible Investment Report

In the past I have not made my technophobic disposition a secret, if I could have my way, I’d probably be writing this with chalk and papyrus. But I would be remiss not to talk about the role of artificial intelligence. The broad economic efficiency gains will be transformative, yet in the ‘cons’ column we can list things like governance, who controls what, the high energy and water requirement, and the potential to replace jobs that would otherwise be done by a human being. In South Africa today, the unemployment rate for graduates with a bachelor’s degree or higher already stands at 10.3%.

Considering the ‘pros’ column, AI’s most immediate impact is being felt through efficiency gains, such as automating routine tasks, optimising supply chains, improving capital allocation and enhancing decision‑making across sectors ranging from manufacturing and logistics to healthcare and financial services. As AI systems absorb and process vast quantities of data at speed, firms are able to reduce operational costs, increase productivity and respond more dynamically to changing market conditions. Over time, these efficiency gains are expected to translate into higher potential growth, shifts in labour demand, and a reconfiguration of competitive advantages at both a corporate and national level. However, these gains are not evenly distributed and come with second‑order effects - including energy intensity, infrastructure demands and skills displacement - that will shape how value is created and captured across the global economy.

For responsible investors, AI represents both a powerful enabler and a material source of risk. On the opportunity side, AI is transforming the depth, quality and usability of ESG data. Machine learning tools can ingest unstructured information — from satellite imagery and geospatial data to corporate disclosures and supply chain records — enabling more granular tracking of emissions, land use change, water stress and social indicators at an asset and portfolio level. This materially improves investors’ ability to assess the physical and transition risks of climate change, monitor progress against emissions glidepaths, and test the credibility of corporate transition plans over time. In practice, this allows responsible investment frameworks to move beyond static snapshots toward dynamic, forward looking assessments that better reflect real world outcomes and transition alignment.

At the same time, the rapid expansion of AI infrastructure introduces new stewardship considerations. Data centres and their associated water and energy demands create tangible environmental externalities that must be actively assessed. Responsible investors therefore have a critical role to play in ensuring that AI driven growth is aligned with climate objectives, rather than becoming a source of unpriced emissions and resource pressure. This includes engaging with companies on renewable energy procurement, data efficiency, governance of AI systems, and transparency around lifecycle impacts. Ultimately, AI has the potential to materially enhance how investors track, measure and influence sustainability outcomes — but only if it is deployed deliberately, governed robustly, and integrated into responsible investment practices as a tool for accountability rather than abstraction.

Data has been a key pillar in our Responsible Investment Framework over the past few years, and its role is only becoming more meaningful with the added ability to make sound inferences and inform strategic decision-making.

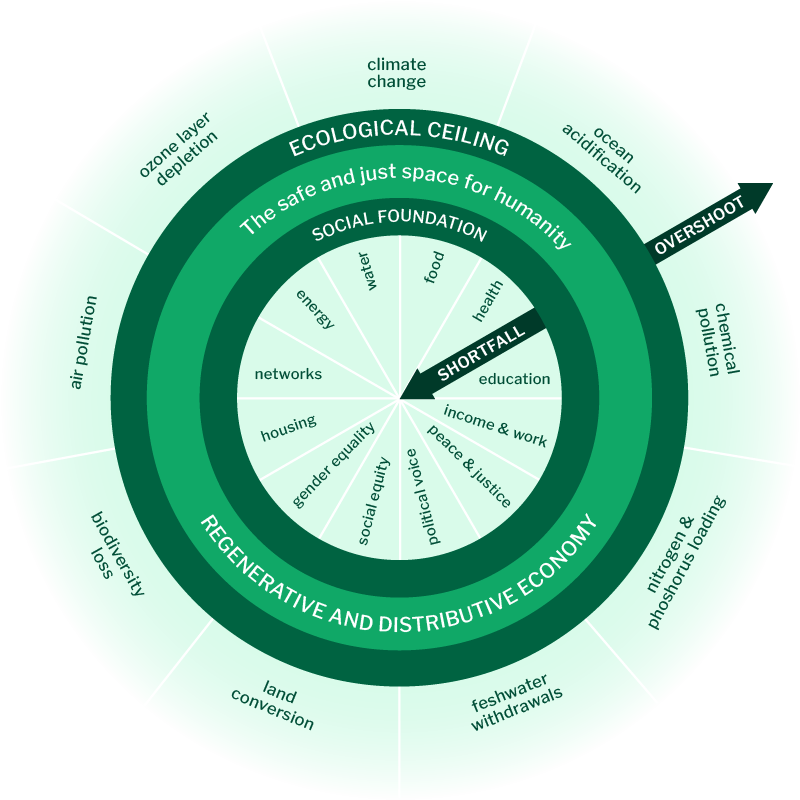

As we move into 2026, much of 2025 was spent self-marking and then refining our Responsible Investment Framework. I also happened to pick up Kate Raworth’s wonderful book again, Doughnut Economics - or Donut Economics, depending on what side of the Atlantic you bought it. Her framework reminded me of the power of imagery - humans have a greater ability to recall visuals than they do text. Raworth has created a wonderful graphic that captures the interplay between Society, the Planet, and the Economy. Which got us thinking, can we apply a similar approach to responsible investing?

Responsible Investment Framework

We have reported in the past on our key sustainability focus areas, namely climate change, biodiversity loss, social equity, and human and labour rights. How these interacted with our Responsible Investment Framework was always a challenge to capture and relay. Our framework was created using the DEAL acronym, made up of Data, Engagement, Active ownership, and Leadership. Where Raworth has used the Sustainable Development Goals and the Stockholm Resilience Centre’s Planetary Boundaries, we have leant into our Sustainability Focus Areas and DEAL Framework.

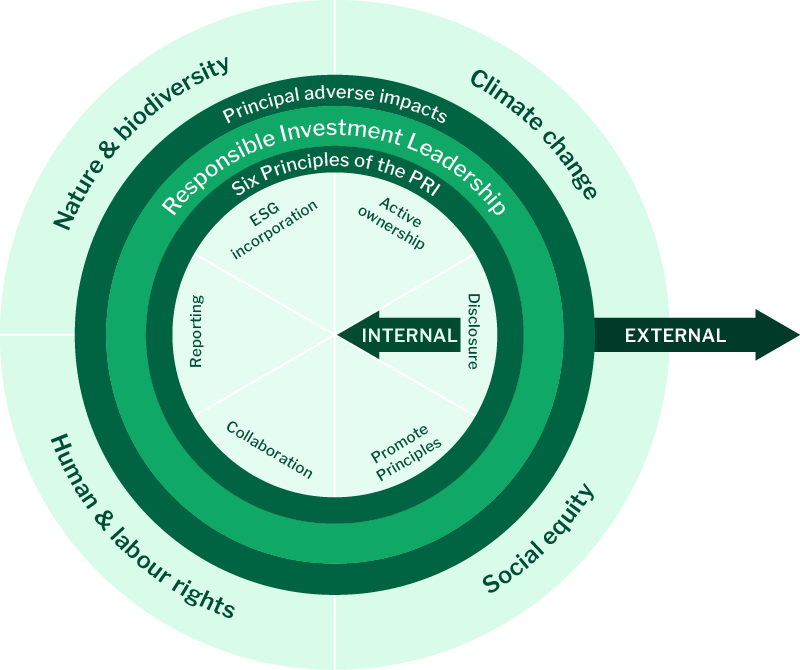

I have also provided a third option which our readers may find useful, many of our contemporaries are signatories to the UN-supported Principles for Responsible Investment, and we can similarly borrow from Raworth’s work here.

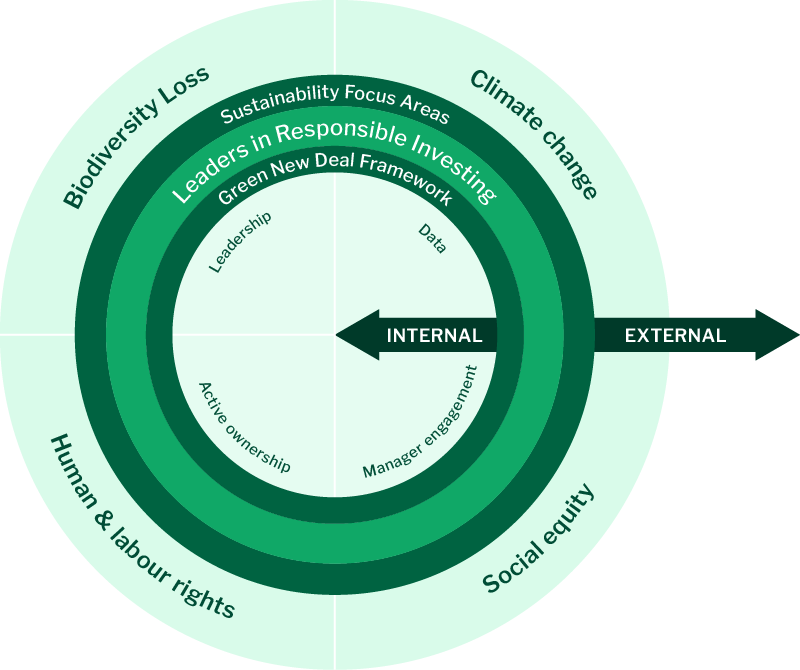

The internal portion of the Nedgroup Investments doughnut utilises our DEAL acronym, which we see as elements within our control. We believe we can move the dial where it comes to leveraging data, engaging with our third-party investment managers, effecting active ownership through our stewardship activities, and leading by working collectively with the asset management industry and its stakeholders.

Looking outside the doughnut, we have our four key sustainability focus areas where we believe our investment activities can have meaningful real-world outcomes. Differing to the internal elements, here we indirectly affect these areas, and through identifying, measuring, and tracking well-considered data points we can better mitigate and manage these risks.

Should we perform well on each pillar with our DEAL elements, we should move outward and into the doughnut, which we define as being leaders in responsible investing. Similarly, as we begin to better manage our adverse impacts and record tangible improvements, we would see climate change, biodiversity, social equity, and human rights move into the responsible investment ring. This is the ‘sweet spot’. And of course, like any sweet spot, as our ambition grows so do our hurdles to achieving responsible investment best practice.

I look forward to reporting on our progress during 2026 and in our future annual reports.

Raworth’s Doughnut of social and planetary boundaries

Getting inside the doughnut using the six principles of the PRI

What getting inside the doughnut looks like for Nedgoup Investments

Source: Kate Raworth (2017), Doughnut Economics: Seven Ways to Think Like a 21st-Century Economist, Nedgroup Investments

Climate transition risks (eventually) become a reality

South Africa’s climate policy landscape, although many years in the making, is beginning to take shape. Moving from the establishment of a formal regulatory framework, through rising carbon pricing, to the resulting investment implications. The three points below highlight the introduction of the Climate Change Act as the legal foundation for a coordinated national response, the implementation of Carbon Tax Phase 2 with higher headline prices but continued relief mechanisms, and the growing relevance of these developments for investment risk, capital allocation and stewardship decision‑making.

Why it matters? First, these policy developments materially increase transition risk for emissions‑intensive sectors, as rising carbon prices and the prospect of enforceable carbon budgets introduce clearer financial consequences for non‑compliance. Second, the continued availability of allowances and offsets means that regulatory exposure will increasingly differentiate between companies with credible long‑term transition strategies and those relying on short‑term mitigation — an important distinction for both portfolio construction and stewardship priorities.

Climate Change Act: Establishing the regulatory framework

South Africa’s Climate Change Act, proclaimed in March 2025, establishes the legal foundation for a coordinated national response to climate change. While sector-specific emissions targets and enforcement mechanisms are still being finalised, the Act already places clear obligations on provincial and municipal authorities to integrate climate adaptation into planning and decision-making processes.

Regulatory impact is expected to intensify as sectoral emissions targets are gazetted. National Treasury has indicated that future carbon budgets may carry material financial consequences, including penalties of up to R640 per tonne for emissions exceeding allowable limits — materially increasing transition risk for high-emitting sectors.

Carbon Tax Phase 2: Higher prices, continued relief

Carbon Tax Phase 2 took effect on 1 January 2026, with the headline carbon price rising to R308 per tonne of CO2e — a 30.5% increase from 2025 levels. This strengthens South Africa’s alignment with international climate commitments and reduces exposure to external measures such as the EU’s Carbon Border Adjustment Mechanism.

However, the 2025 National Budget softened previously proposed tightening. The 60% basic tax-free allowance was extended to at least 2030, and earlier proposals to raise trade-exposure thresholds were abandoned.

As a result, while carbon costs are rising, the overall regime remains relatively accommodative, with offsets expected to remain a key tool for managing liabilities.

Investment implications: managing transition risk and opportunity

The evolving climate policy landscape has direct implications for investment risk, capital allocation and stewardship priorities. Rising carbon prices, the prospect of enforceable carbon budgets, and potential penalties for noncompliance are likely to increase cost pressures and valuation risks for emissions-intensive sectors.

At the same time, the availability of allowances and offsets underscores the importance of credible, long-term transition plans rather than short-term emissions management.

From an investment perspective, this reinforces the need to distinguish between companies proactively aligning strategy, capital investment and governance with a lower-carbon economy, and those facing escalating regulatory and financial risk - shaping both portfolio decisions and stewardship activity.

Climate adoption in asset management

Incorporating climate considerations into portfolio management is increasingly central to the effective assessment of long‑term risk and return. Climate change introduces both physical risks — such as extreme weather events, water stress and supply‑chain disruption — and transition risks, arising from policy shifts, technological change and evolving consumer preferences. These risks are already influencing asset valuations, cost of capital and corporate competitiveness across sectors and regions. For investors with long‑dated liabilities, understanding how climate risks are embedded within portfolios is therefore critical not only to preserving value, but also to ensuring that capital allocation decisions are aligned with a transitioning real economy. Importantly, climate considerations are not static; they evolve as regulation tightens, technologies scale, and corporate strategies diverge, reinforcing the need for ongoing, forward‑looking analysis within portfolio construction and risk management.

Against this backdrop, our annual fund manager climate survey is designed to deepen our understanding of how climate risks and opportunities are being measured, managed and integrated at both the issuer and portfolio level. A core focus of the survey is identifying which emission factors managers are measuring and tracking — including Scope 1, 2 and, where feasible, Scope 3 emissions — as robust, decision‑useful data is foundational to assessing exposure, comparing issuers and monitoring progress over time. Granular emissions data enables investors to move beyond headline carbon metrics toward a clearer view of portfolio‑level emissions trajectories, emissions intensity and alignment with credible decarbonisation pathways.

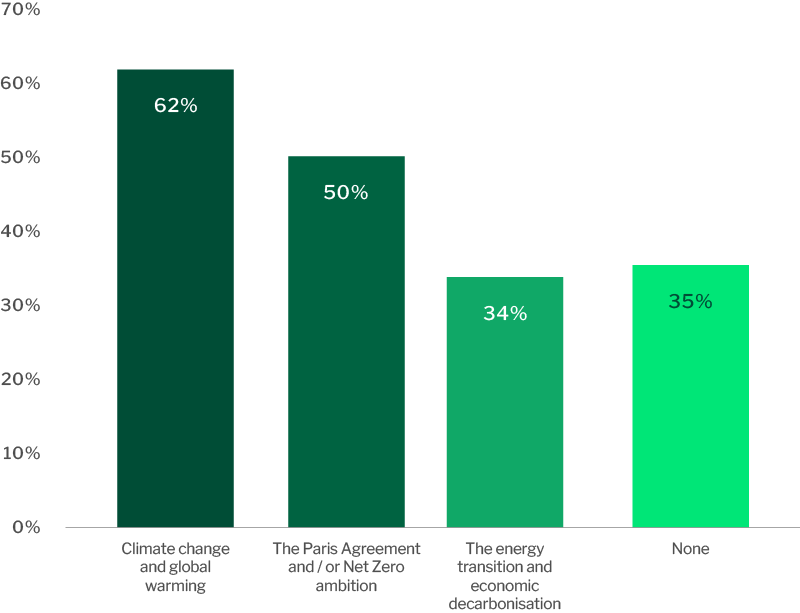

Policy statements are a public declaration of ambition and intent, and are a key component of the PRI’s assessment as it applies to the commitment of signatories. The right-hand chart shows the proportion of our partner managers whose ESG-related policies explicitly recognise climate considerations. It indicates that climate change and global warming are the most commonly acknowledged themes, followed closely by references to the Paris Agreement or net‑zero ambitions, suggesting growing alignment with international climate frameworks. Taken together, the data highlights clear progress in policy acknowledgement, but also underscores an important opportunity to move from broad climate recognition towards more specific, investment‑relevant commitments linked to transition pathways and decarbonisation outcomes. In her section titled ‘Building climate resilience’, my colleague, Keletso Mphomane, has illustrated what this means in practice.

Portion of active equity assets that recognise various climate considerations in their policies

Source: Nedgroup Investments, December 2025

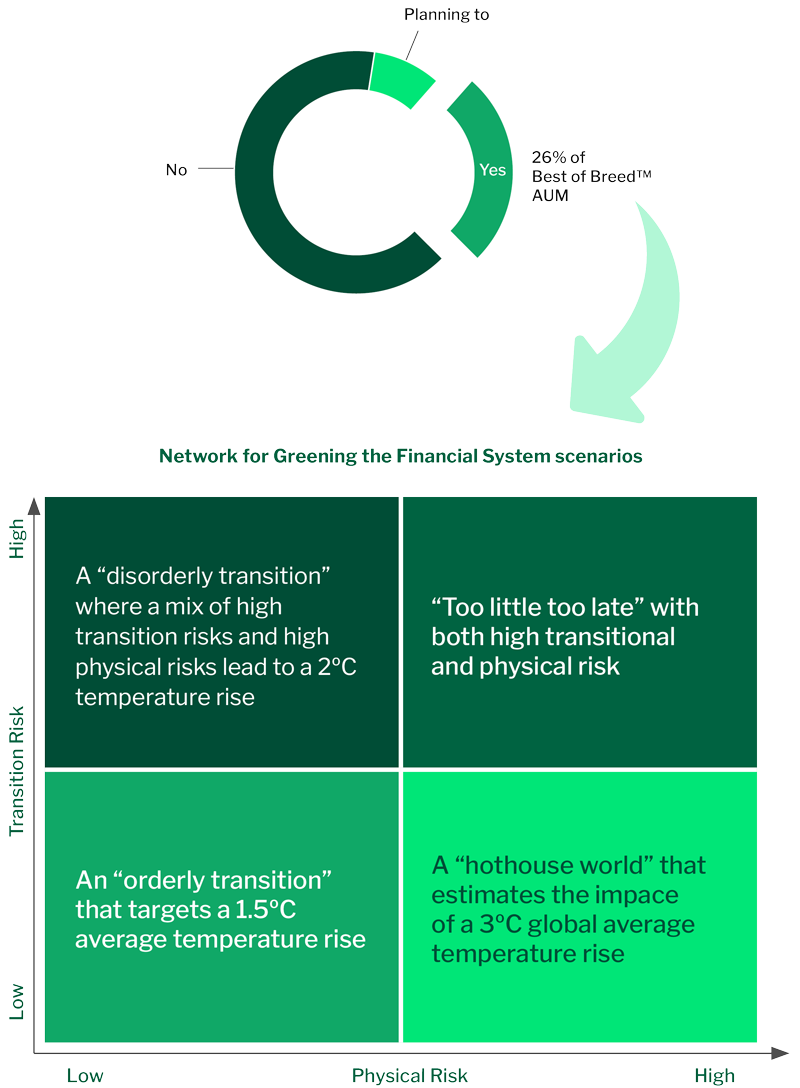

The survey goes on to examine whether managers have incorporated emission reduction targets and transition objectives into their investment strategies, recognising that targets provide an important signal of intent, accountability, and strategic coherence. In addition, we assess the extent to which managers are using climate transition scenario analysis to stress‑test portfolios under different policy, temperature and technology outcomes. Scenario analysis is a valuable tool for understanding how assets may perform as the transition accelerates, highlighting potential areas of vulnerability as well as opportunity. Collectively, these insights allow us to evaluate not only how climate risks are currently being managed, but how well portfolios are positioned for a range of plausible future outcomes — informing engagement priorities, stewardship activity and long‑term capital allocation decisions.

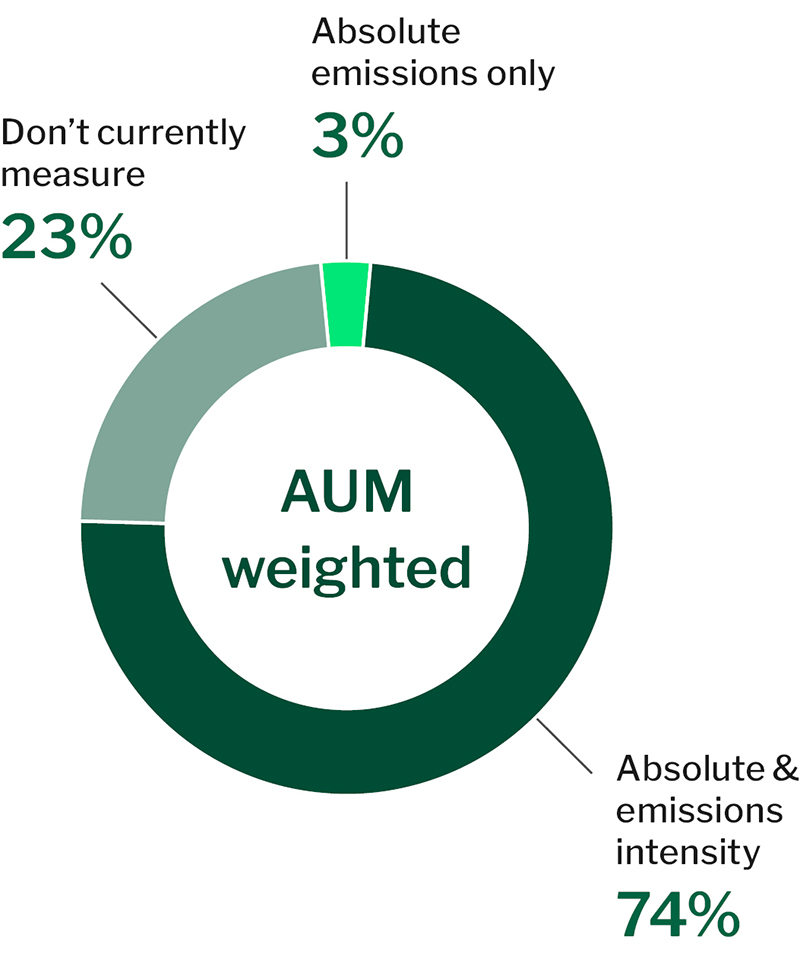

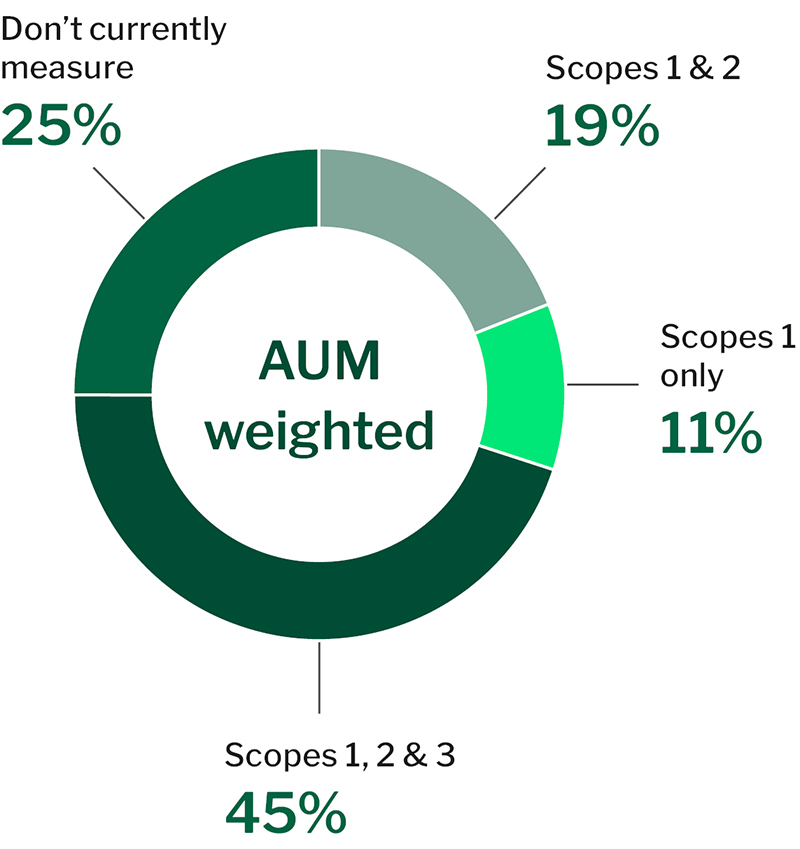

The two charts below illustrate the current state of climate measurement and target‑setting practices across our network of fund managers. The pie charts suggest that a majority of assets are now covered by some form of greenhouse gas measurement and portfolio carbon footprinting, yet work remains to incorporate the remaining quarter of our assets.

Asset Management 2025 Climate Survey

Do you measure greenhouse gas emissions of investee companies?

Do you measure the carbon footprint of your portfolios?

Source: Nedgroup Investments, December 2025

Do you have any climate-related targets at a portfolio level?

Source: Nedgroup Investments, December 2025

The area chart reinforces this picture by highlighting a clear gap between measurement and action: a significant proportion of actively managed assets are managed without any portfolio‑level climate targets, with only a smaller subset aligned to net‑zero or explicit emissions‑reduction objectives. Taken together, the data suggests that while climate data availability and disclosure have improved materially, these insights are not yet consistently translated into forward‑looking targets or portfolio constraints.

These results are not unique to our survey and are a reflexion of the global market. Many local and global managers have highlighted the complexity with setting targets that meet ambition, pragmatism, and agility, while taking into consideration sector and regional context. What the results do point to is the need for the industry to better apply its mind in this regard, as the absence of clear targets risks limiting accountability, reducing decision‑usefulness, and slowing the integration of climate considerations into investment and stewardship outcomes.

Do you conduct climate scenario analysis for your portfolios?

Source: Nedgroup Investments, December 2025

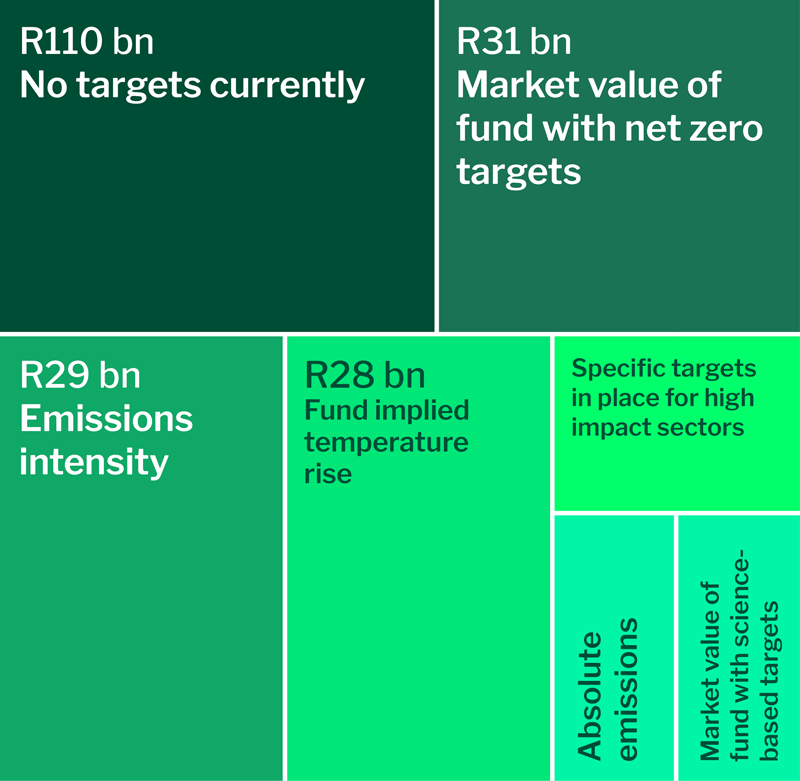

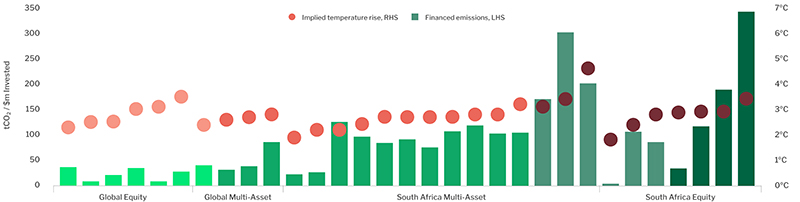

Nedgroup Investments emissions profile

Financed emissions have emerged as a critical lens through which investors can assess their true exposure to climate risk and their contribution to real‑world emissions outcomes. Unlike operational emissions, which reflect the footprint of an asset manager’s own activities, financed emissions capture the greenhouse gas emissions associated with the companies and assets in which capital is deployed. As the below chart suggests, financed emissions refers to the tonnage of carbon dioxide attributed to a $1million worth of investment. This perspective is increasingly important as it aligns investment analysis with the drivers of climate transition risk, recognising that long‑term portfolio performance is influenced by how investee companies adapt to decarbonisation pressures over time.

Reflecting this shift, emerging international reporting standards — including the IFRS sustainability disclosure framework — are placing greater emphasis on the measurement, disclosure and use of financed emissions data. By bringing funded emissions into the core of climate reporting, IFRS is reinforcing the expectation that investors move beyond high‑level commitments and demonstrate how climate considerations are embedded within investment decision‑making, risk management and stewardship.

Implied Temperature Rise (ITR) is a forward‑looking metric that translates a portfolio’s current and projected emissions profile into an estimated global temperature outcome, based on the alignment of underlying holdings with climate pathways. Rather than measuring emissions in isolation, ITR provides a forward‑looking view of whether portfolio companies are on track to meet decarbonisation trajectories consistent with internationally agreed climate goals.

In a portfolio management context, this enables investors to assess transition alignment across assets, identify areas of heightened risk, and compare portfolios on a like‑for‑like basis. Lowering a portfolio’s implied temperature over time is typically achieved through a combination of levers: engaging with investee companies to strengthen transition strategies and emissions targets, reallocating capital towards more resilient and transition‑aligned businesses, and integrating climate transition considerations into portfolio construction and monitoring. Used consistently, ITR becomes a practical tool for tracking progress, informing engagement priorities and demonstrating how portfolios are evolving in line with a transitioning real economy.

Nedgroup Investments fund range climate snapshot

Source: MSCI data, Nedgroup Investments, December 2025

Conclusion

My hope is that you find this report both insightful and informative, in that it gives you a good insight into how we at Nedgroup Investments think about Sustainability, Stewardship, and Responsible Investing. My colleague Keletso has showcased how portfolios can build in resilience, which Tumisho has built on in her segment on how asset management can achieve purpose at scale. Leonard sits on our proxy voting decision committee and has wonderfully articulated the role that voting plays within his passive investing business. Madhushree considers deeply and philosophically about the arms manufacturing sector and how this is an increasingly delicate terrain into today’s geopolitical landscape.

As per the past few years, we end our report by inviting you to read through some of the case studies and corporate engagements that our partner managers have enacted over the course of 2025.

Although nothing beats a face-to-face conversation, by disclosing this information and being transparent in our work, we hope our clients and stakeholders are armed with a decent amount of information to engage with the topic and challenge us on these important areas. In falling prey to the old adage, I firmly believe that responsible investing is one of those spaces where a rising tide does indeed lift all boats.

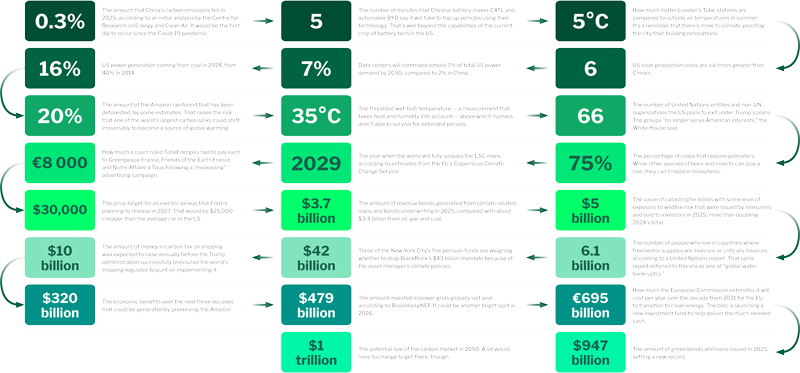

2025: A world in numbers

Source: Bloomberg Green, December 2025