A cornerstone of responsible investment and effective stewardship

Related links

Read the full 2025 Responsible Investment Report

The rapid growth of passive investing has reshaped global capital markets. Index-tracking funds now account for a substantial share of equity ownership in many listed companies, making passive investors among the largest and most stable shareholders worldwide. Passive strategies can’t sell. So what’s their real power lever? One vote. Index funds may track benchmarks, but they don’t track governance. When passive investors vote, they can influence corporate behaviour, uphold fiduciary responsibilities, and climate accountability - and because they often hold companies for as long as they remain in an index, that influence compounds over time.

Passive ownership does not mean passive stewardship

A common misconception is that passive investing equates to a hands-off approach to corporate governance. In reality, the structural features of passive strategies — broad market exposure, long-term holding periods, and limited ability to divest — arguably strengthen the case for robust stewardship. Passive investors are effectively “universal owners”, exposed to economy-wide risks such as climate change, social instability, and governance failures that can undermine long-term market returns. If you own “the market,” you inherit systemic risk, and you can’t diversify away from it. So what does this mean in practice? It means engagement and voting are not optional extras, but essential tools for protecting and enhancing long-term value across portfolios when you can’t exit the position.

Proxy voting provides the formal channel through which passive investors exercise these ownership rights. Through votes on director elections, executive remuneration, capital allocation, and shareholder resolutions, asset managers can signal expectations around governance standards, sustainability performance, and risk oversight. In many cases, voting is the clearest and most visible expression of stewardship, particularly when engagement alone has failed to drive progress.

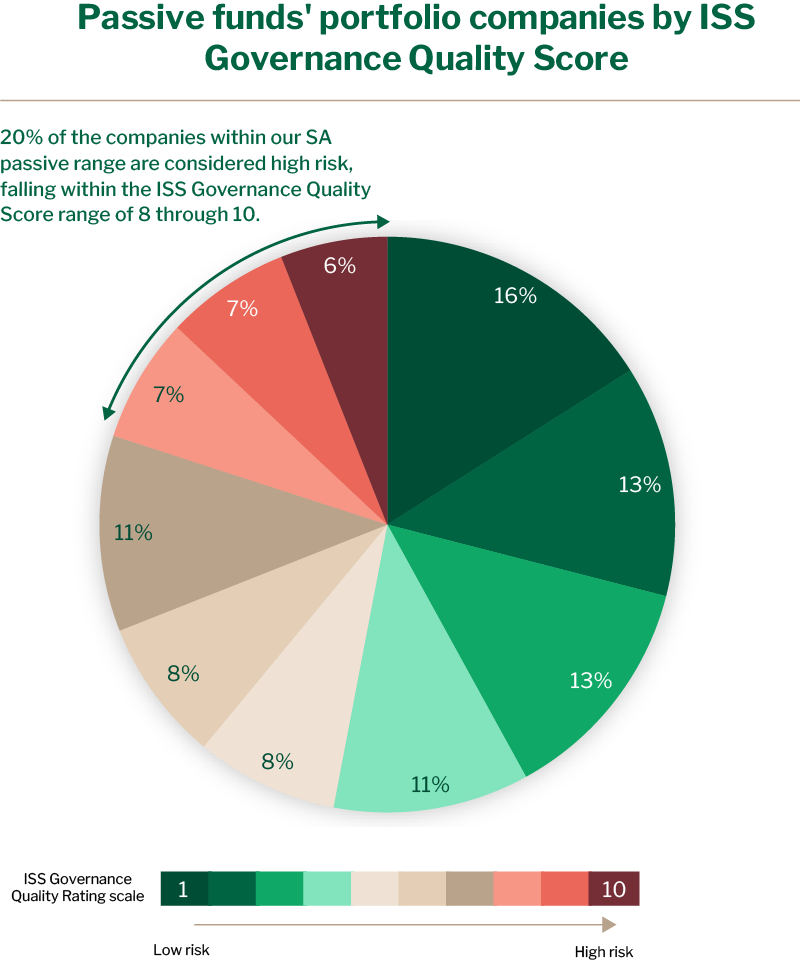

Source: ISS, Nedgroup Investments, December 2025

Enacting responsible investment through voting

Responsible investment frameworks emphasise the integration of environmental, social, and governance (ESG) considerations into investment analysis, ownership practices, and decision making. For passive investors, proxy voting is the primary means of translating these principles into action. While index trackers do not tilt portfolios based on ESG scores, they can — and increasingly do — use voting to promote better disclosure, stronger governance, and improved management of material sustainability risks.

Votes on climate transition plans, board diversity, supply chain standards, and shareholder rights have become central to how asset owners assess stewardship quality. Importantly, proxy voting allows passive managers to pursue market wide improvements rather than company specific exclusions, aligning with their mandate to track broad indices while still addressing systemic risks. In this sense, voting acts as a bridge between passive portfolio construction and active ownership responsibilities.

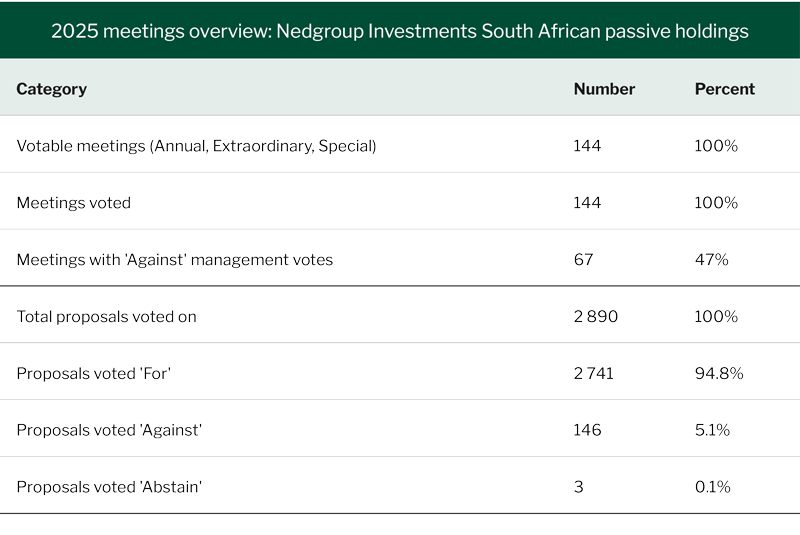

Source: ISS, Nedgroup Investments, December 2025

Why proxy voting matters more in passive than active strategies

The importance of proxy voting is amplified in passive strategies precisely because exit is not a credible tool. Active managers may respond to poor governance or weak ESG performance by reducing or selling a holding. Passive managers, by contrast, remain invested for as long as a company is included in the index. Voting — particularly when combined with sustained engagement — becomes the primary lever for influencing outcomes.

Moreover, the scale of passive ownership means that voting decisions by large index managers can materially affect shareholder outcomes. Support or opposition from major passive holders often determines whether resolutions pass, whether directors are re-elected, and how boards interpret investor expectations. With that influence comes heightened responsibility: passive stewardship has real-world consequences.

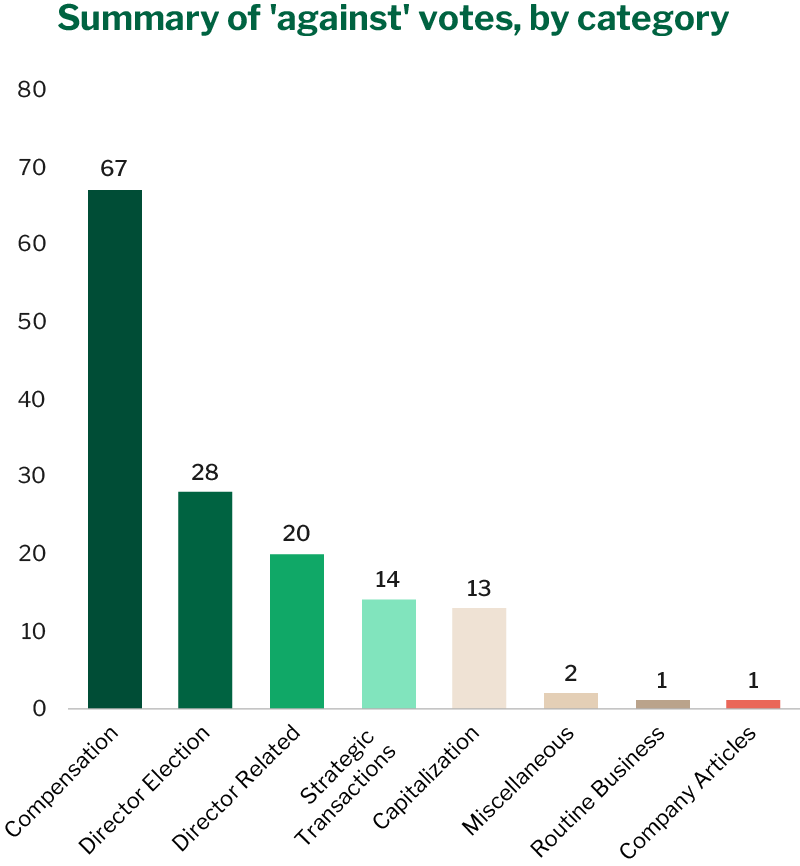

Source: ISS, Nedgroup Investments, December 2025

Accountability, alignment, and transparency

As scrutiny of stewardship practices has intensified, asset owners and beneficiaries increasingly expect clear evidence that proxy voting is aligned with stated responsible investment policies. Disclosure of voting records, rationales for key decisions, and escalation frameworks has become a baseline expectation. Misalignment between voting behaviour and public commitments — particularly on climate and governance issues — can undermine credibility and trust.

Recent developments such as pass through or client directed voting reflect growing demand for greater alignment between asset owners’ preferences and how votes are cast on their behalf. Operationally complex or not, the trend reinforces the central point: voting connects end investors to real-world corporate outcomes.

Proxy voting as a foundation of effective stewardship

Ultimately, proxy voting is not a box ticking exercise, nor a substitute for engagement. It is most effective when embedded within a broader stewardship framework that includes ongoing dialogue, clear escalation pathways, and collaboration with other investors. For passive managers, voting reinforces engagement by adding accountability and consequences — particularly when votes against management signal dissatisfaction with progress on material risks.

In an investment landscape increasingly shaped by passive strategies, proxy voting has become one of the most powerful tools for influencing how companies are governed and how they respond to long-term sustainability challenges. Far from being passive actors, index investors play a defining role in shaping corporate behaviour across markets. Exercised thoughtfully and transparently, proxy voting ensures that passive investing remains compatible with responsible investment objectives and effective stewardship — helping safeguard value not just for individual portfolios, but for the financial system as a whole.