SARB seeks clear evidence of a sustained decline in inflation

Related links

No related links

On 28 May 2026, the South African Reserve Bank’s (SARB) Monetary Policy Committee (MPC) raised the repo rate by 25 basis points, taking the policy rate to 7.00%, effective 29 May 2026. While the outcome was broadly in line with market expectations, the decision was not unanimous. Four MPC members voted in favour of the increase, while two preferred to leave rates unchanged. This split highlights the difficult balance the Committee is attempting to strike between containing inflationary pressures and limiting downside risks to sustainable economic growth.

The decision comes amid elevated global uncertainty, driven in part by the ongoing conflict in the Middle East and continued disruption around the Strait of Hormuz, which accounts for roughly 25% of global oil trade. With oil prices trading near $100 per barrel and broader inflation concerns re-emerging globally, expectations for near-term monetary easing in major economies have also receded. Against this backdrop, the SARB has adopted a more proactive stance aimed at preserving the credibility of its inflation-targeting framework, while acknowledging that the current shock is largely supply-driven.

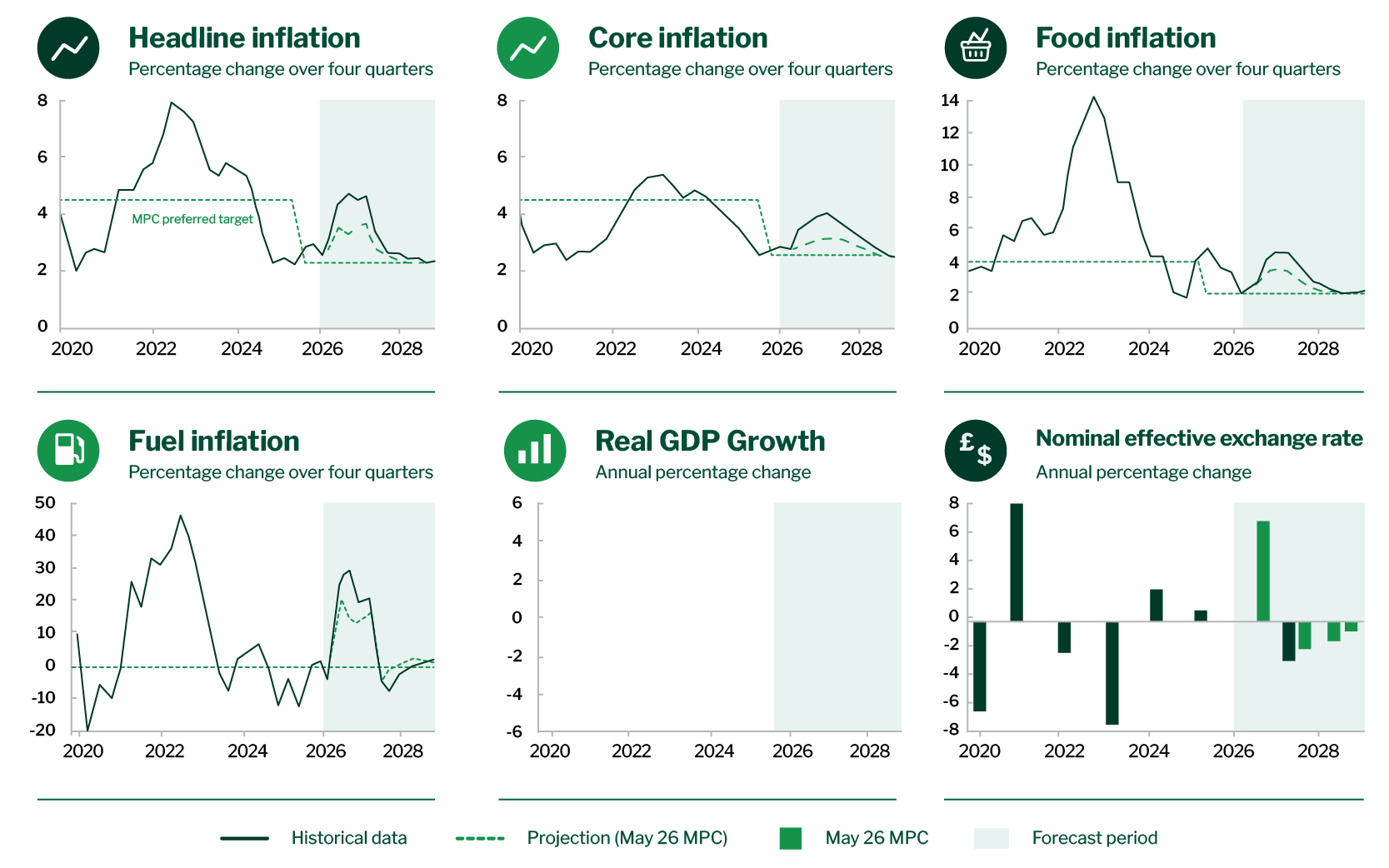

Although the rand remains stronger than it was a year ago, helping to contain imported inflation, and food inflation has shown some recent moderation, the SARB continues to flag upside risks to the inflation outlook. Headline CPI rose to 4.0% in April, driven largely by a sharp increase in fuel prices, while services inflation accelerated to 4.6%, suggesting that price pressures are becoming more broad-based. Reflecting these developments, the Bank revised its inflation forecasts higher relative to the March meeting. Headline inflation is now projected at 4.4% for 2026, up from 3.7%, and 3.7% for 2027, up from 3.3%, while the 2028 forecast remains unchanged at 3.0%. Although clear second-round effects are not yet evident in the data, the MPC noted that both market-based and analyst inflation expectations have begun to drift higher, increasing the risk that the current shock becomes more persistent through wages and broader price-setting behaviour.

At the same time, the SARB lowered its growth forecasts, reflecting the stagflationary character of the current macroeconomic environment. Real GDP growth is now expected to average 1.2% in 2026, down from 1.4% previously, and 1.7% in 2027, down from 1.9%, while the 2028 forecast remains unchanged at 1.9%. The weaker outlook reflects a combination of heightened uncertainty, pressure on household purchasing power, and softer investment conditions, alongside the impact of recent flooding in parts of the country. Importantly, the MPC emphasised that risks to growth remain tilted to the downside, despite some resilience in the domestic economy through improved sentiment, ongoing reform efforts, and relatively supportive terms of trade.

Finally, the SARB’s Quarterly Projection Model (QPM) continues to suggest that the tightening cycle may be nearing its peak, with the baseline estimate implying one additional 25 basis point increase in the second half of the year, followed by a gradual easing path as inflation moderates. That said, the MPC was clear that this path should be viewed as indicative rather than prescriptive, with future policy action remaining firmly data dependent.

Figure 1: SARB selected forecasts

Source: SARB, Taquanta Asset Managers

Fund positioning

Our cash and income funds remain well positioned for the current hiking cycle. The portfolios are primarily invested in floating-rate instruments, meaning coupon income will reset to the new, higher rates over the coming weeks and months. This should provide welcome support to income investors, who continue to benefit from inflation-beating returns while maintaining relatively low levels of liquidity, duration, and credit risk.