What ZARONIA and FLAC mean for investors

Related links

No related links

South Africa’s money market industry is undergoing one of its most significant structural shifts in decades, driven by two concurrent reforms: the transition from the long‑standing Johannesburg Interbank Average Rate (JIBAR) to the new South African Rand Overnight Index Average (ZARONIA), and the implementation of Financial Loss Absorbing Capacity (FLAC) instruments.

ZARONIA

As the South African Reserve Bank (SARB) phases out JIBAR in favour of a more transparent, transaction-based benchmark by 2026, ZARONIA is reshaping how cash, liquidity, and floating rate instruments are priced across the financial system.

At the same time, the introduction of FLAC—loss absorbing instruments required by regulation for systemically important banks—represents a fundamental change in capital structure, creditor hierarchy, and risk allocation within the banking sector. FLAC instruments, mandated under Prudential Standard RA03 effective January 2026, aim to enhance financial stability of systemically important banks and reduce reliance on taxpayer funded bailouts by ensuring that private investors absorb losses in any bank distress resolution. Together, these reforms signal a re-pricing of risk, new liquidity behaviours, and a reconfiguration of funding markets, with implications for cash investors, money market funds, issuers, and treasury operations.

JIBAR (Johannesburg Interbank Average Rate) has long been used as a benchmark for short-term interest rates in South Africa. JIBAR is essentially the average rate at which banks in South Africa are willing to lend unsecured funds to each other for a specific term. A panel of major South African banks submits bid and offer rates (i.e. borrowing and lending rates) for different maturities. Outliers are removed (typically top and bottom 20-25%. The remaining mid-rates are averaged. This produces the official JIBAR rate for that tenor.

ZARONIA is calculated from actual overnight transactions in the South African market. It uses executed transactions between banks and other financial institutions and has no reliance on estimates or quotes. It is a purely historical rate.

It is important to note that JIBAR is quote-based (what banks say they would lend at) and ZARONIA is transaction-based (what actually traded). JIBAR can be influenced because it’s opinion-based. ZARONIA is robust because it’s evidence-based. As a result, ZARONIA is less susceptible to manipulation risk unlike JIBAR.

JIBAR is expected to be discontinued in December 2026. In support of this transition, an industry-wide initiative is underway to ensure that no new JIBAR-linked instruments are issued beyond May 2026. The regulator further anticipates that all outstanding JIBAR-linked exposures will be transitioned to ZARONIA by year-end.

ZARONIA: Key implications for South African Fixed Income

The shift to ZARONIA is expected to have fairly minimal impact on portfolios, as increased market transaction volumes have stabilised differences between the forward-looking JIBAR rate and the transaction based ZARONIA benchmark.

A key distinction between JIBAR and ZARONIA lies in their respective sensitivity to interest rate expectations. JIBAR, being a forward-looking term rate, typically adjusts in anticipation of expected changes in monetary policy. As such, it may trend upward or downward ahead of actual adjustments by the South African Reserve Bank (SARB) to the repo rate, reflecting prevailing market expectations of future interest rates. When investing in an instrument linked to 3-month JIBAR, the applicable interest rate is fixed at the outset of the period and remains known for the full three-month duration.

ZARONIA, by contrast, is a transaction-based rate that reflects realised overnight funding costs. While it updates daily in line with market activity, it can also reprice immediately following monetary policy decisions. For example, in the event of a rate cut by the Monetary Policy Committee (MPC), ZARONIA, as an overnight rate, will adjust on the same day to reflect the new policy rate. This dynamic may result in greater day-to-day variability in fund yields.

Taquanta Asset Managers has begun participating in ZARONIA-linked instruments and will continue to assess opportunities for client portfolios as market liquidity and issuance develop further.

In preparation for the transition away from JIBAR, Taquanta is undertaking a structured readiness programme, including updates to valuation frameworks, recalibration of benchmark curves, and enhancements to interest rate risk tools to appropriately reflect the daily sensitivity of a transaction-based reference rate.

In parallel, the team is engaging with banking counterparties, industry working groups, and broader market participants to remain informed of evolving market conventions and funding dynamics, and to ensure that client portfolios are positioned in a measured and considered manner as ZARONIA adoption progresses.

FLAC

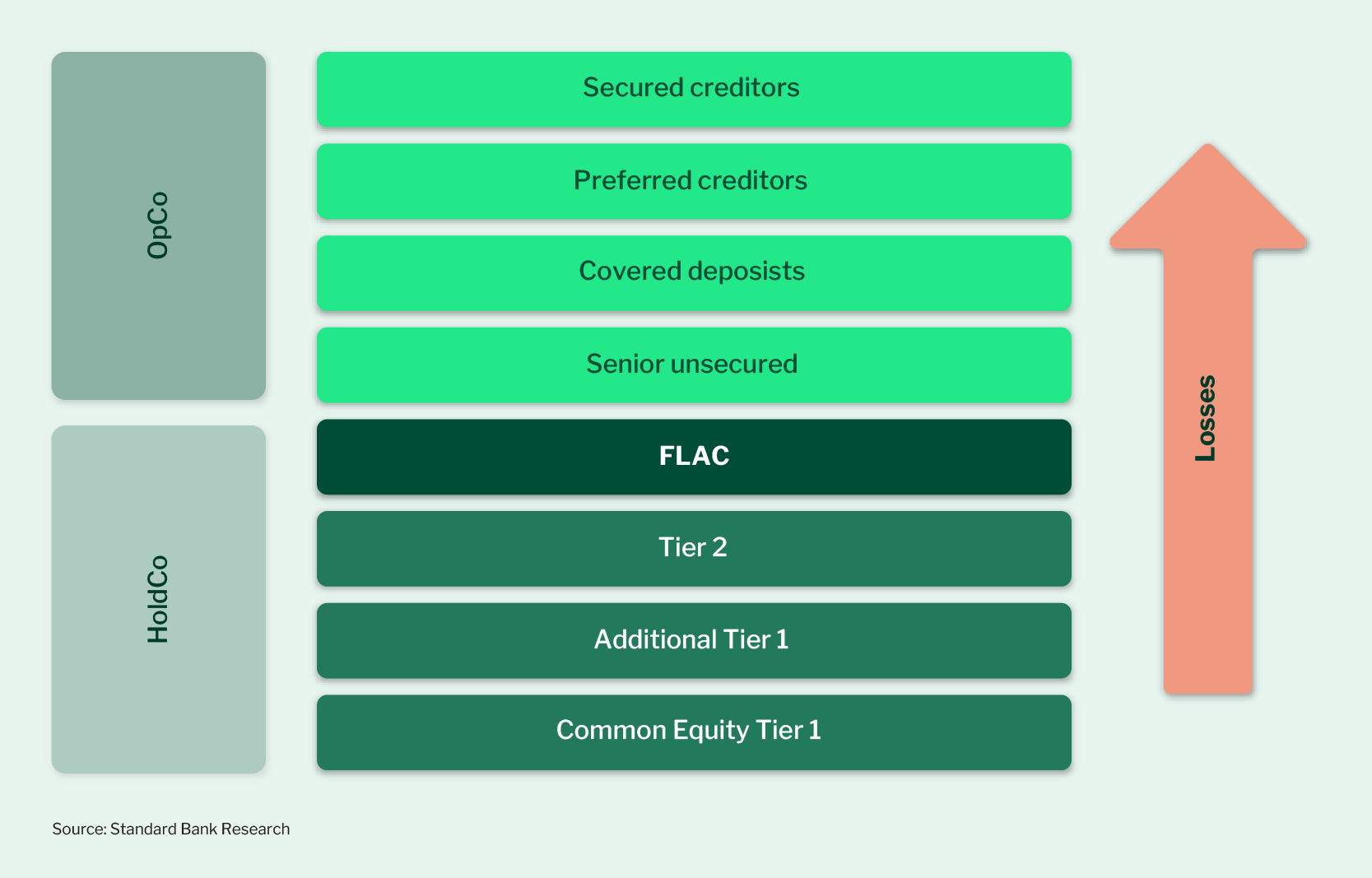

FLAC are loss-absorbing bank instruments which are subordinate to other forms of senior debt such as deposits, and senior to regulatory capital. Typically, FLAC is issued out of the bank’s holding company. They are designed to absorb losses after regulatory capital is depleted (CET1, AT1, T2) but before operating company senior liabilities are affected. This is aligned with the South African resolution framework, where loss-absorbing capacity is structurally positioned at the holding company level. In a resolution scenario, losses are absorbed at the holding company, thereby protecting depositors and senior creditors at the operating bank level.

The purpose of FLAC (Funding Loss Absorbing Capacity) is to support the orderly resolution of a potentially distressed bank without recourse to taxpayer-funded bailouts. It provides an additional, dedicated layer of loss-absorbing capacity that can be utilized to absorb losses during periods of financial stress, thereby enhancing the resilience of the institution and offering an added layer of protection to senior creditors.

Figure 1: Simplified Creditor Hierarchy

Source: Standard Bank Research

Given FLAC’s position within the creditor hierarchy, any investment would need to provide adequate compensation for the additional loss-absorbing risk - typically pricing at a premium to senior unsecured debt, while remaining below that of Tier 2 and Tier 1 capital instruments.

FLAC instruments: Key implications for South African Fixed Income

The introduction of FLAC marks a structural shift in South Africa’s bank funding landscape. The SARB estimates that systemically important banks will need to issue FLAC to the value of approximately R288–R360 billion FLAC. The issuance of these instruments will cause a meaningful change in the type of instruments issued by banks and may partially crowd out traditional senior unsecured issuance.

In principle, FLAC instruments should offer a spread premium to senior unsecured debt, reflecting their explicit bail-in and subordination risk. However, early market pricing suggests that FLAC is currently trading at levels close to senior unsecured debt, implying that investors are not yet being adequately compensated for the additional risk and reduced liquidity. This mispricing is a key area of focus and may reflect the cash flush environment together with anaemic SA GDP growth. The introduction of FLAC may support tighter spreads on senior unsecured debt and NCD issuance, as the additional loss-absorbing layer enhances structural protection for senior creditors.

From a portfolio construction perspective, FLAC is not a substitute for traditional senior bank paper. Its explicit resolution risk and structural features make it less suitable for cash and short-duration mandates with strict liquidity and capital preservation requirements. In particular, FLAC instruments are unlikely to qualify for inclusion in money market funds under CISCA constraints, given their effective tenor profile. As such, the natural investor base is expected to be enhanced income, income, and credit strategies.

While FLAC strengthens systemic resilience by improving loss absorption, reducing moral hazard, and supporting orderly bank resolution, it may introduce additional spread volatility as the market establishes appropriate pricing, particularly in stressed conditions.

Taquanta's view

FLAC introduces a valuable new layer of bank credit exposure, but current pricing does not adequately reflect the underlying risks. We remain cautious in the near term and will only allocate where spreads sufficiently compensate for bail-in and liquidity risk. FLAC is best suited to mandates with the flexibility to absorb volatility. Key Considerations for Portfolio Managers:

• Adequacy of spread premium vs senior unsecured debt

• Market liquidity and depth over time

• Behaviour under stressed market conditions

• Alignment with mandate constraints and regulatory limits

• Risk-adjusted return relative to alternative credit opportunities

Ultimately, successful participation in the FLAC market will depend on disciplined credit selection, appropriate mandate alignment, and a clear assessment of whether pricing adequately compensates for the additional risks.