From risk to legacy: Why great advice is about behaviour

Related links

No related links

In an environment dominated by market headlines, geopolitical uncertainty and short‑term noise, it is easy to assume that volatility is the greatest threat to a client’s financial plan. Yet history tells a very different story. Financial plans generally don’t fail because markets underperform. Far more often, they fail because human behaviour intervenes at exactly the wrong moment.

When clients speak about “risk”, they are almost never talking about volatility, standard deviation or drawdowns. They are speaking emotionally, not technically. Clients worry about whether their plan will work, whether they will be financially secure, and whether their family will be taken care of. This emotional definition of risk is very different from the academic or investment definition fund managers and advisers are trained to think in, and yet it is the one that matters most at key decision‑making moments.

Therefore, the true value of advice does not lie in predicting markets or identifying the next winning asset class, but in helping clients make consistently good decisions over long periods of time.

The real risks that derail financial plans

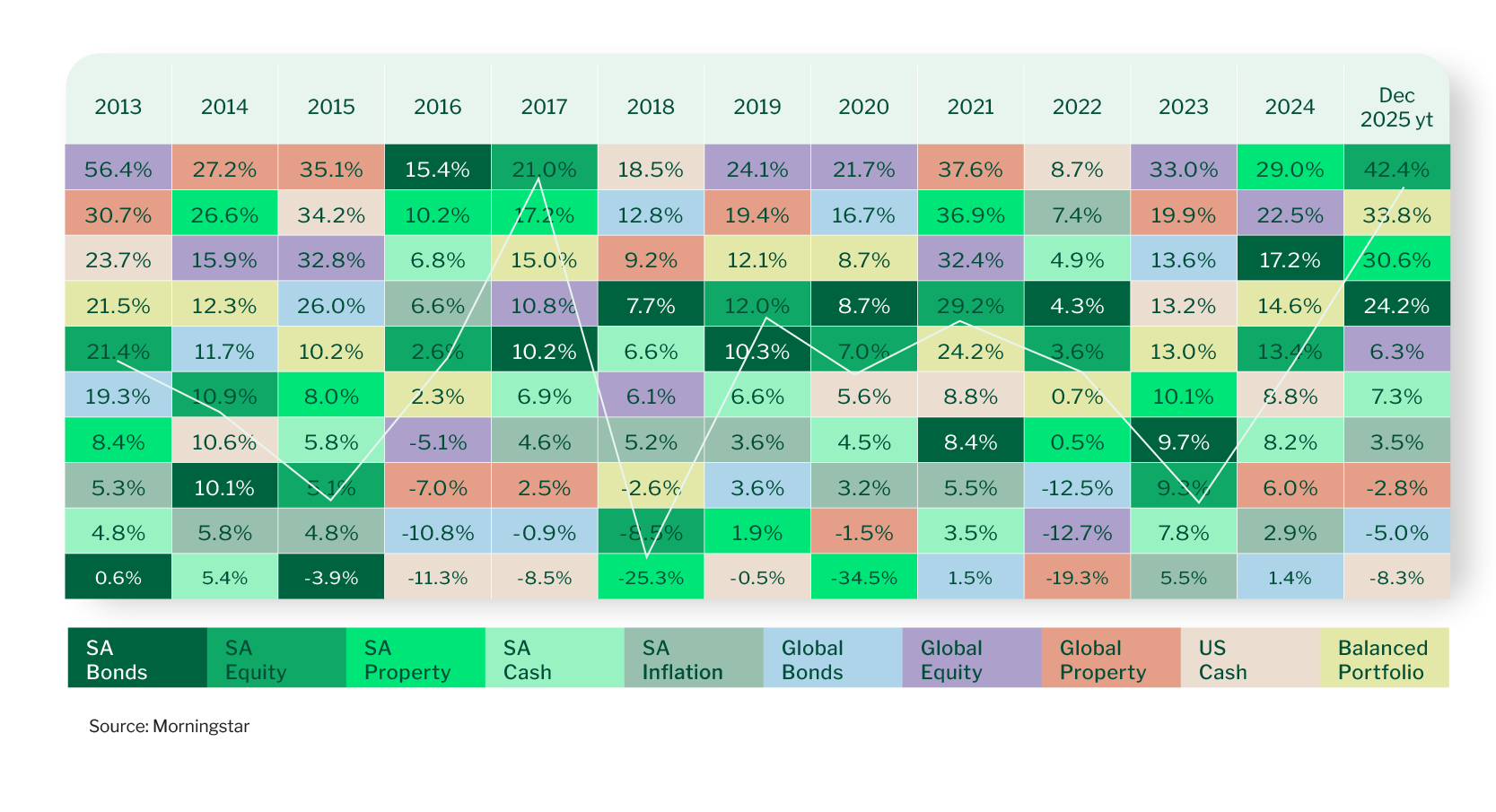

In practice, three risks show up repeatedly in clients decision making. Timing risk arises when clients delay investing while waiting for the “right time”, forfeiting the most valuable years of compounding. Reaction risk appears when clients react emotionally to volatility by stopping contributions or switching out of growth assets after losses have already occurred. Concentration risk creeps in when familiarity or recent success leads clients to place too much trust in a single manager, asset class or region.

These emotional risks quietly erode outcomes even in portfolios that are otherwise well constructed. Crucially, none of them are solved by better market forecasts. They are solved by better client decisions.

Time: The most underestimated risk‑management tool

Time in the market is one of the simplest and most effective risk‑management tools available, yet it is frequently overshadowed by debates around contribution levels or return assumptions.

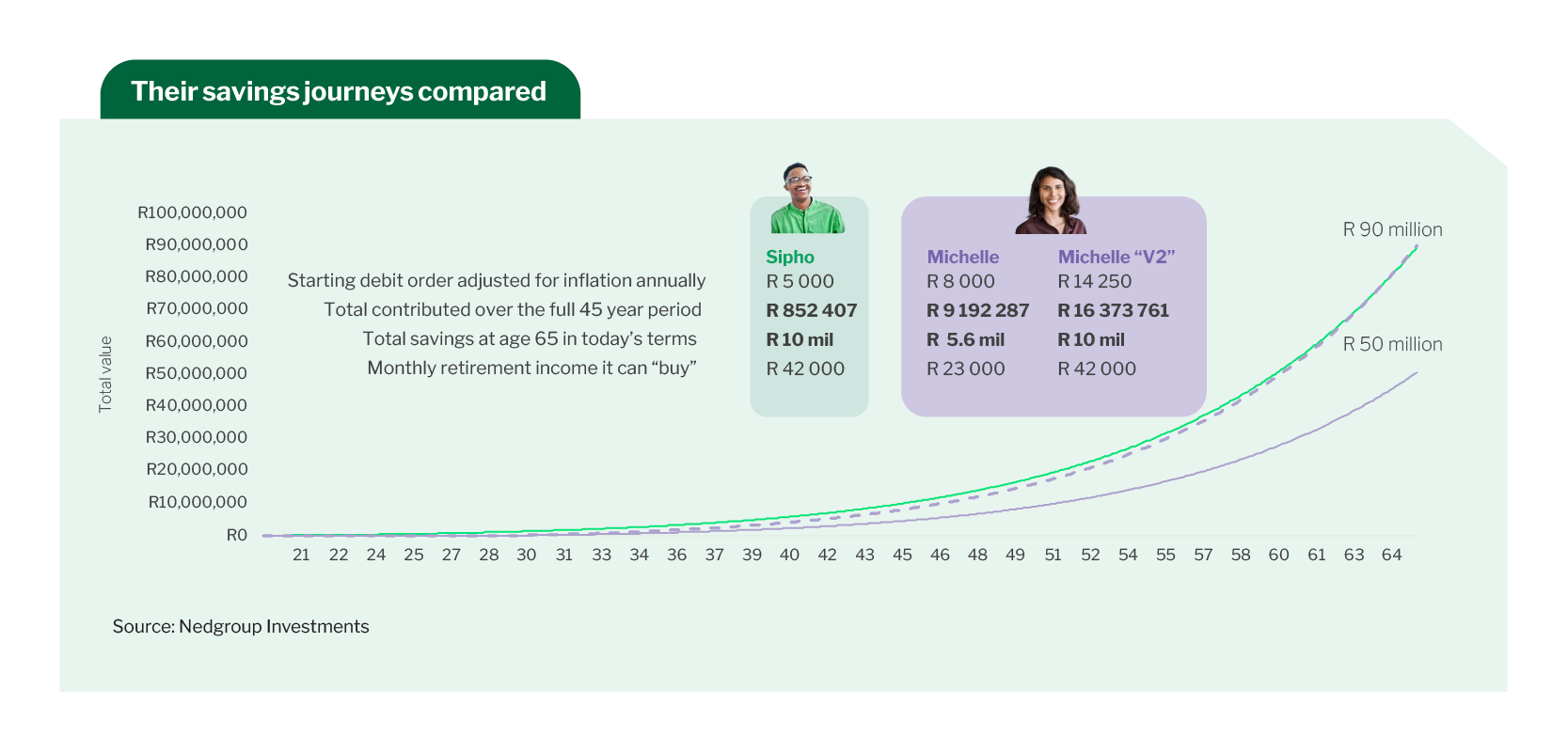

Consider a simple illustration. Sipho and Michelle make very different choices early in life. Sipho starts saving at age 20 and contributes for just ten years. At 30, he stops contributing and focuses on family and lifestyle, but leaves his investments untouched. Michelle, by contrast, only starts saving at 30, contributes more each month than Sipho ever did and continues saving diligently for 35 years.

Despite her discipline, Michelle never catches up. Sipho’s early start gives compounding time to do the heavy lifting, especially in the final years before retirement when portfolio values are largest. Michelle is forced to work harder and contribute materially more than what Sipho did for the same or worse outcome. The lesson is clear - start now. It really is about time in the market and not timing the market.

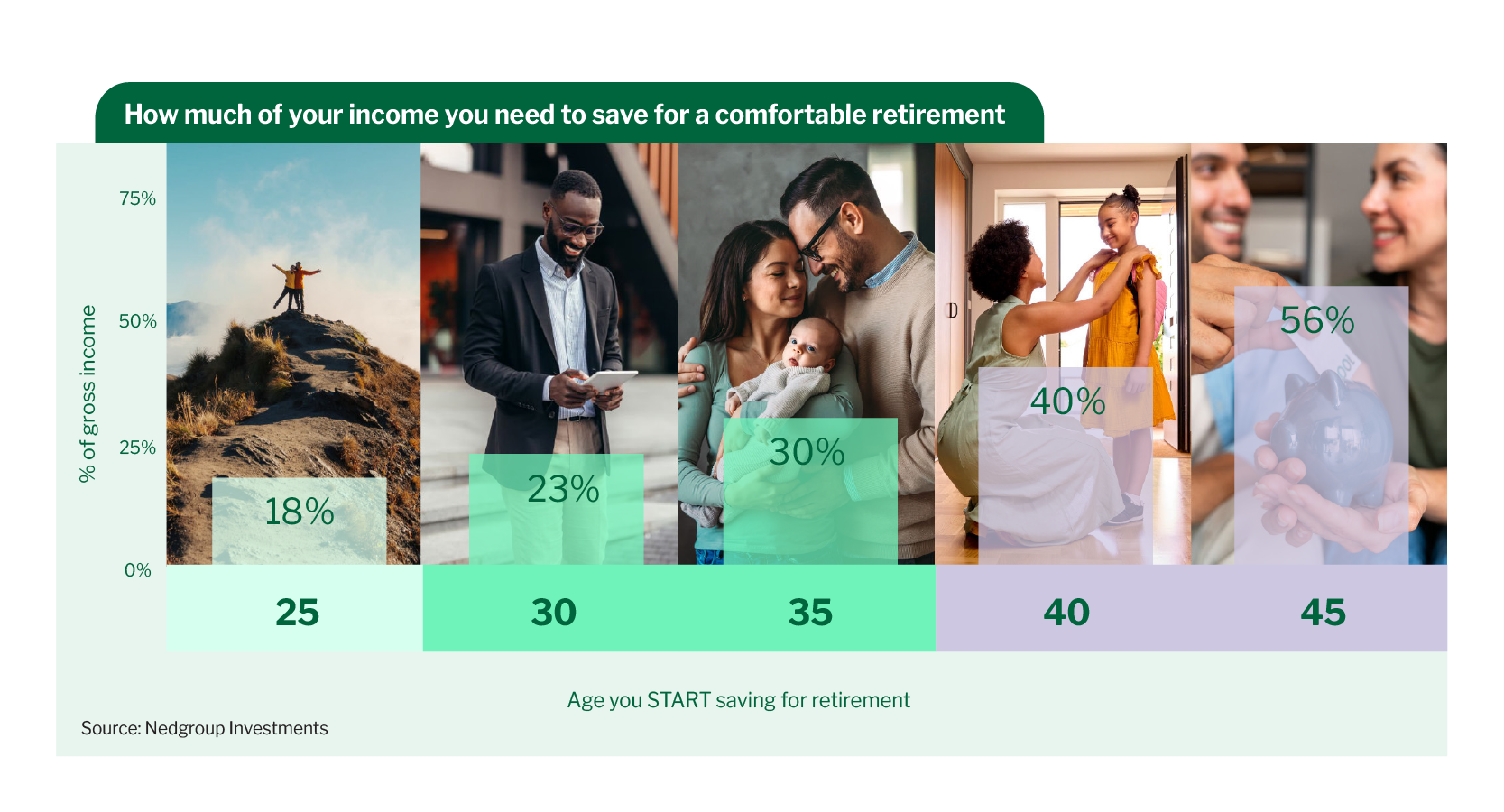

This dynamic is particularly damaging in retirement planning. Younger clients often believe they cannot afford to save meaningfully while they are building their careers. But income growth usually comes hand‑in‑hand with expense growth. As people move through life, financial commitments multiply rather than disappear.

The mathematics of retirement saving highlights this trade‑off unambiguously. Starting early means smaller sacrifices over time, while delaying saving pushes the burden into later years when clients aren’t able to absorb it. Helping clients understand this early is one of the most valuable interventions an adviser can make.

Volatility is inevitable, behaviour is a choice

While delayed investing is one threat, emotional decision‑making during market volatility is another. Volatility is not an anomaly in markets; it is a permanent feature of growth assets. Equity markets have always experienced large swings in the short term, and they always will.

The danger lies not in those swings themselves, but in how clients respond to them. This is where advisers add the most value. During turbulent periods, clients do not need clever tactics or confident forecasts. They need perspective, reassurance and a structure that prevents them from making permanent mistakes in response to temporary events.

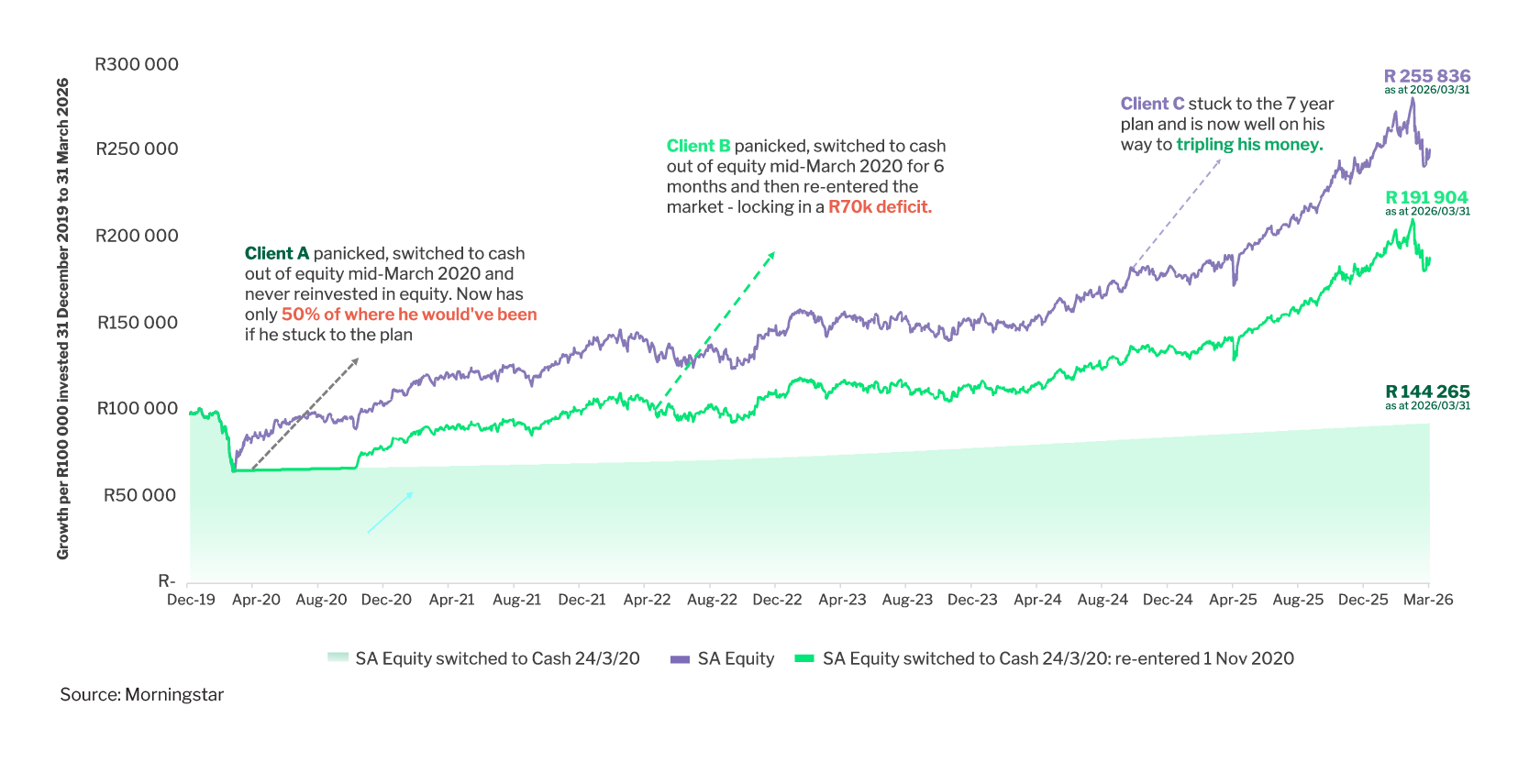

The chart below illustrates this clearly. Three clients began with the same 7-year plan at the start of 2020, yet their outcomes diverged purely because of behaviour. One client abandoned equity and never returned, ending up with roughly half of the value they could have had. Another panicked, moved to cash briefly and re‑entered later, permanently locking in a meaningful shortfall. Only the client who stayed invested throughout remained on track to achieve their original objective — and ultimately compound their wealth significantly. The message is again simple but powerful: markets recover, but poor decisions compound just as reliably.

Concentration risk: When familiarity becomes a threat

Another risk that frequently undermines well‑intentioned financial plans is concentration, or recency bias. Clients naturally gravitate towards what has worked recently — a strong‑performing asset class, a favoured geography or a trusted fund manager. Yet markets have consistently shown that leadership rotates. The asset class or manager that leads performance in one period is often among the laggards in the next. Concentrated portfolios therefore amplify both investment risk and behavioural stress, increasing the likelihood that clients lose confidence, chase performance or abandon underperforming exposures at exactly the wrong time. From an advice perspective, diversification is not only about spreading investment risk; it is about reducing the emotional pressure points that make good decision‑making hardest.

Using Portfolio Structure to Support Good Behaviour

Ultimately, the role of a financial plan is three-fold: protect near-term spending needs, grow long-term purchasing power and reduce the chance of a big behavioural mistake. Its purpose is to support good decision‑making at each stage of a client’s life. Early on, that means making saving easy and allowing time to do the work. During busy family years, it means building resilience so clients remain committed despite competing demands. As retirement approaches, it means managing volatility and avoiding poorly timed decisions, while in retirement it means sustaining income without unnecessary complexity or stress. A well‑constructed plan is as much about behaviour management as it is about investment outcomes.

Turning risk into legacy

Ultimately, great advice transcends products and markets. At its core, advice is about guiding clients through uncertainty with discipline, structure and perspective. It is about helping them stay invested when emotions urge them not to, and keeping their plans intact through the inevitable ups and downs of markets and life.

Markets will always fluctuate and headlines will always unsettle. But advisers who focus as much on behaviour as they do on asset allocation give their clients something far more valuable than short‑term certainty. They give them the best possible chance of turning risk into something enduring: a legacy.