Quality investing isn’t dead. But the way it gets defined might be.

Related links

No related links

Backward-looking definitions of quality offer investors false comfort. A more durable approach requires a sharper focus on resilience, valuation and long‑term relevance, argues Nisha Thakrar.

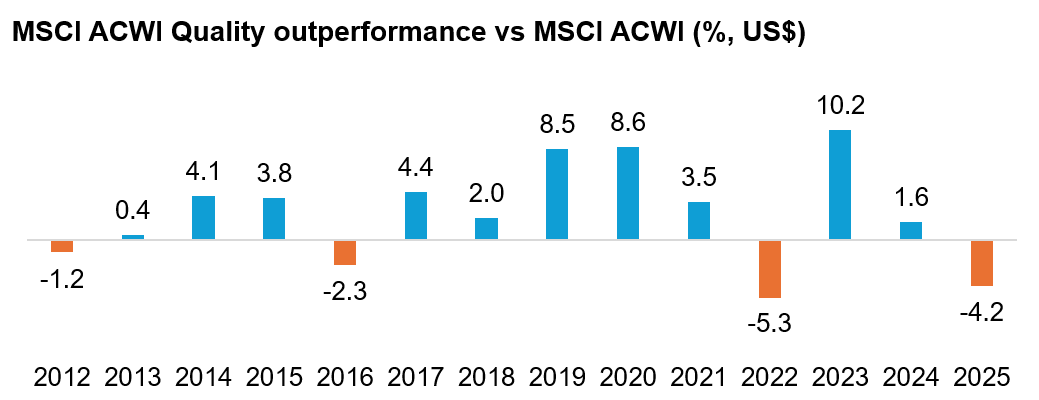

After a successful decade, quality investors ended 2025 on softer ground. The style trailed the broader equity market (based on MSCI ACWI) by more than 4% as a risk‑on rally pulled capital out of high‑quality names into more speculative growth stocks.

The move wasn’t unprecedented – 2022 was an even tougher year – but it was a reminder that style leadership shifts with macroeconomic conditions. When uncertainty dominates, predictable earnings growth is prized; when momentum takes over, risk‑taking often eclipses quality.

Source: MSCI, December 31, 2025

Should investors see this is as a temporary setback? Or should they view this as a sign that traditional frameworks reliant on screenable metrics, such as high returns on equity, earnings stability and low leverage, are no longer enough? While investors should not lose faith in quality investing, we do think it is time to consider more durable approaches.

Durability cannot be found in screens

Screens tell us where a business has come from, but they say far less about where it is going. Durability requires an understanding of the core business and the ecosystem around it: how defensible are its revenues, does it have pricing power and, crucially, what could go wrong? Consider a streaming company. Its peers are no longer just other streamers; it’s all other forms of digital entertainment which are competing for users’ time.

In-depth research is, therefore, essential – but it must be paired with discipline. Knowing where not to spend time is just as important as knowing where to do more work.

Binary outcome dependencies are a clear red flag. A pharmaceutical company deriving most of its revenues from a single blockbuster drug facing patent expiry may look profitable today, but its future earnings power could be highly fragile. Similarly, a semiconductor manufacturer reliant on a handful of large customers may exhibit strong margins yet be vulnerable to forces beyond its control, such as shifts in bargaining power or capital cycles.

Secular decline presents an equally important challenge. Some industries face structural questions about their long-term relevance. In such cases, historical profitability offers little protection when the economic foundations are eroding.

Many firms have well-resourced research capabilities. Far few embed the long-term mindset and intellectual honesty required to separate structural change from short-term noise. That discipline is increasingly tested in volatile, narrative-driven markets.

Artificial intelligence is an obvious example. There is little doubt AI is transformative, not just for the enablers but across industries. Yet investor attention has narrowed to the hyperscalers, with little differentiation between them. This is where durability and valuation intersect. Even high quality businesses can become mispriced when narratives overpower fundamentals.

Price matters, even for quality stocks

Seven of the ten largest holdings in the MSCI ACWI Quality Index also feature in the top ten constituents of the broader MSCI ACWI. This convergence reflects years of superior earnings growth, and the premium investors have been willing to pay for it. The rise of passive flows, pod shops and retail investors have only amplified this concentration, pushing large capital pools towards the mega caps.

However, strong past performance does not eliminate valuation risk. The real opportunity in quality investing lies in recognising durability before consensus does. Given the recent shift in market structure, we see that further down the market cap.

Speciality chemicals are a case in point. The industry is often dismissed because of its association with commodity chemicals. Yet speciality chemicals are higher margin, less cyclical and structurally more resilient. Misunderstood industries, management missteps or cyclical downturns can all push durable businesses out of favour. The key is recognising when long‑term earnings power is being mispriced.

Even the strongest businesses experience uneven growth. What distinguishes a quality business is how it builds resilience; this could be through a broader range of customers and end-markets, a balance of recurring and cyclical revenues or management teams capable of navigating different phases of growth.

Quantitative frameworks tend to penalise this non-linear growth, excluding businesses whose earnings path is uneven despite strong underlying fundamentals. This is precisely why in-depth research and a long‑term mindset matter.

The bottom line

Quality investing does not require rigid rules or narrow definitions. It requires a framework that consistently seeks durability – in business models, earnings power and long-term relevance.

The opportunity is rarely uncovered by chasing the usual suspects, but through identifying companies whose future potential remains underappreciated.

This article reflects the views of Nedgroup Investments and is intended for informational purposes only. It does not constitute investment advice or a recommendation to buy or sell any financial instruments. All investments involve risk.

‘This article was originally published in Institutional Asset Manager.’